Creating a family budget doesn’t have to be overwhelming or complicated. In fact, the simpler your budget is, the more likely it is that your family will stick to it. Budgeting is a powerful tool that helps reduce stress, improve communication between family members, and set you on a clear path toward financial freedom.

Let’s break down exactly how to build a practical and effective family budget — even if you’ve never budgeted before.

Why Every Family Needs a Budget

A family budget serves as a roadmap for your money. It helps you understand where your income is going, how to save for goals, and how to prepare for the unexpected. Without a budget, it’s easy to overspend or fall behind on savings.

Key reasons to budget:

- Reduce unnecessary spending

- Save for emergencies, education, and retirement

- Prevent money-related stress in the household

- Make sure bills are paid on time

- Work toward shared family goals

Step 1: Know Your Total Household Income

Start by calculating how much money your family brings in each month. This includes:

- Salaries (after taxes)

- Freelance or side hustle income

- Government benefits

- Child support or alimony

- Any other regular income

Be honest and realistic. If your income fluctuates, take an average from the last 3–6 months to get a more accurate picture.

Step 2: Track Every Expense for 30 Days

Before you can cut costs or set goals, you need to know where your money is going. For one full month, track every expense:

- Fixed expenses (rent, utilities, insurance, debt payments)

- Variable expenses (groceries, gas, entertainment, clothes)

- Irregular or annual expenses (school supplies, birthday gifts, vacations)

Use a spreadsheet, an app like Mint or YNAB, or even a notebook. The key is consistency.

Step 3: Categorize and Organize Your Spending

Once your spending is tracked, group your expenses into categories. Here’s a simple layout:

- Needs (50%): rent, mortgage, utilities, groceries, transportation

- Wants (30%): dining out, subscriptions, hobbies

- Savings/Debt Repayment (20%): emergency fund, retirement, loans

This is based on the 50/30/20 rule, which is flexible and beginner-friendly. You can adjust the percentages to fit your family’s situation.

Step 4: Set Clear Financial Goals

Now that you know your income and spending habits, it’s time to create short- and long-term goals.

Short-term goals (3–12 months):

- Build a $1,000 emergency fund

- Pay off one credit card

- Save for holiday gifts

Long-term goals (1–5+ years):

- Save for a down payment

- Fund college savings

- Pay off student loans or mortgage

Goals provide motivation and give your budget a purpose beyond simply “saving money.”

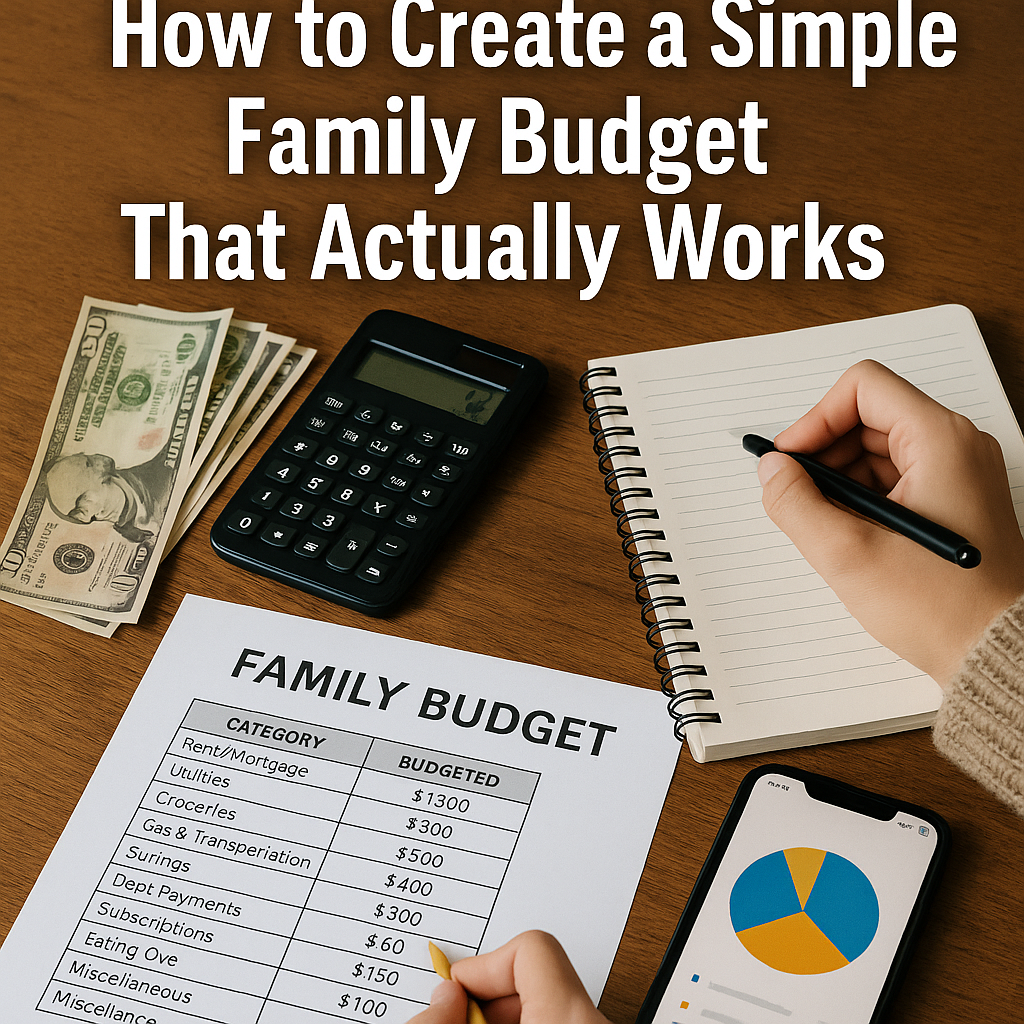

Step 5: Build Your Monthly Budget

Using all the information you’ve gathered, it’s time to create your budget. Write down your income and allocate amounts to each category.

Example:

| Category | Budgeted Amount |

|---|---|

| Rent/Mortgage | $1,200 |

| Utilities | $300 |

| Groceries | $500 |

| Gas & Transportation | $200 |

| Subscriptions | $60 |

| Eating Out | $150 |

| Savings | $400 |

| Debt Payments | $300 |

| Miscellaneous | $100 |

The total should not exceed your monthly income. If it does, look at ways to cut back on “wants.”

Step 6: Choose a Budgeting Method

There are many budgeting systems, so pick one that feels right for your family:

- Zero-Based Budgeting: Every dollar has a job. Income – Expenses = $0.

- Envelope System: Use cash envelopes for categories like groceries or entertainment.

- 50/30/20 Rule: Simple and easy to implement.

- App-Based Budgeting: Digital tools for automated tracking and syncing with accounts.

Try a method for a few months before switching. What matters most is that everyone sticks to it.

Step 7: Hold Monthly Family Budget Meetings

Sit down with your spouse or entire family at least once a month to review the budget. Celebrate wins, talk about setbacks, and make adjustments.

This improves transparency and keeps everyone involved, even the kids — who can start learning smart money habits early.

Step 8: Automate What You Can

Automating bill payments, savings transfers, and even investments removes human error and ensures consistency.

Automation also helps avoid late fees and builds healthy financial habits with less effort.

Step 9: Build in Some Flexibility

Life happens. Medical bills, car repairs, and school fees can throw your plan off course. That’s okay. A good budget is flexible, not rigid.

Re-evaluate and update your budget when:

- Your income changes

- You reach or adjust your goals

- Life events occur (moving, new baby, job change)

Step 10: Stick With It and Don’t Give Up

Budgeting is not always easy in the beginning, but it gets better with practice. Your first few months might feel off — that’s totally normal.

Stay consistent. The long-term payoff is worth it: reduced stress, better financial security, and a stronger foundation for your family’s future.

Final Thoughts: Make Your Budget Work for You

A family budget isn’t about restricting your lifestyle. It’s about giving your money direction and creating a life that aligns with your values and goals. The simpler it is, the more likely you are to keep using it.

Take it one step at a time. Start small, be honest, involve your family, and build a financial plan that brings peace of mind — not pressure.